What Happens After You Refinance Your House – If you need a loan to finance the purchase of a property, invest in a business or educate your children, you may experience delays due to the current tight credit environment.

But if you have a home that has been mortgaged for several years, you can actually benefit from the increased market value of the home and apply for a new loan from the bank.

What Happens After You Refinance Your House

The new mortgage, called a mortgage refinancing, will use real estate as collateral to service or settle the existing mortgage, explained U Chen Hock, group head of retail banking at RHB Banking Group.

Should I Refinance My Mortgage? Beginner’s Guide To Refinancing Your Home Loan

Let’s e.g. Suppose a borrower’s existing mortgage has been with bank A for ten years and has fifteen years remaining. The original loan amount of RM300,000 was repaid to RM200,000. The borrower can consider refinancing the mortgage by taking out a new mortgage with Bank B for the remaining RM200,000. The new loan amount of RM200,000 will be used to: Pay off the original loan to Bank A.

The maximum loan term for the new mortgage can be up to 35 years or when the borrower turns 70, whichever comes first.

If additional money is needed, borrowers can actually request a higher refinance amount, provided they meet the new bank’s financing margin requirements, U adds.

‘It’s based on two factors. Firstly, the principal amount you have paid over the years, viz. RM100,000 using the example above. Secondly, an assessment of the value of your assets or both factors,” U explains.

Mortgage Refinance Checklist

Ken Liew, Head of Wealth Advisory (Mortgage) at Financial Group, gives the following example: “Suppose you took out a home loan of RM500,000 20 years ago. Today, the loan up to RM200,000 has been repaid and the property value is increased to RM800,000. You can now apply for a new mortgage from another bank, using the property as collateral to settle the RM200,000 balance. You can withdraw cash up to RM600,000.”

The payout money can be used for business capital, home improvement costs, children’s education funds and even to purchase another property, he says.

“As per Bank Negara Malaysia guidelines, the repayment period for cash payments is limited to 10 years, although some banks may approve periods of more than 10 years if the borrower has good repayment capacity,” Liew added.

The most common reason to refinance is to take advantage of lower interest rates, Liew says. The current low interest rate environment offers great opportunities to refinance loans, he added.

Should You Refinance Your Property?

“You can enjoy a lower interest rate while keeping the remaining term of your original loan. This results in lower monthly costs compared to before,” he explains.

Meanwhile, note that one of the benefits of mortgage refinancing is that the process can be used to consolidate multiple loans into one, appropriate to the borrower’s ability to repay.

“Mortgage products have evolved over the years and you can refinance to take advantage of the latest mortgage features, namely the flexi feature, which allows you to prepay at any time to save interest and then withdraw the advance amount on the next walk. “It is necessary,” he added.

However, Liew does not recommend that borrowers refinance their loans if the remaining term of the original loan is less than 10 years or if the interest rate difference is minimal.

How To Refinance Your Home

“Refinancing mortgages costs a lot of money, including bank processing fees, stamp duty, appraisal fees and legal fees, so the original loan is almost gone and the new interest rate is less than 1% of the original,” he said. .

You also remind borrowers that they may face fines. “If the original loan had a lock-in period, repayment of the loan may result in termination penalties, as stated in the original proposal. “This is a common mistake when considering mortgage refinancing,” he points out.

In addition, there is a risk that Mortgage Reducing Term Assurance (MRTA) premiums will become more expensive or that insurers will deny coverage because borrowers must apply for a new MRTA for new mortgages. participation

You also note that there are common misconceptions about mortgage refinancing. For example, borrowers often assume that they will automatically qualify for a new mortgage if they can repay their existing mortgage properly.

The Complete Guide To Mortgage Refinancing And How It Can Help You

However, this is not always true. The bank will assess the applicant’s performance and ability to repay the new loan to ensure that it does not become an unnecessary burden. The goal is to exchange your current mortgage for a new mortgage with a lower interest rate. Build assets faster.

The best way to refinance is to know the most common mistakes and how to avoid them. This is what you need to do:

The most important part of refinancing your home is finding the lowest interest rate. This will maximize your savings and make refinancing your home more valuable.

But that’s only part of the equation. There are several strategies you can use to get the most out of your refinancing. Here are some best practices you can follow:

Refinancing: When And How To Refinance Your Purchase Money Mortgage

Your credit history is one of the most important criteria lenders review when you begin the mortgage refinancing process.

If your credit score increases by 1 point, from 679 to 680, your borrowing costs can be reduced by 1 point. That’s $1,000 per $100,000 borrowed.

Eliminating errors with a quick rescore can increase your credit score by up to 100 points in less than a week.

In a recent survey of nearly 6,000 consumers, more than a third of participants discovered errors in their credit reports. And nearly 12% of survey participants discovered errors that could impact their loan rates.

The Benefits Of Cash Out Refinancing

The higher the interest rate, the higher your monthly costs and long-term costs on your new home loan. Therefore, it is in your interest to identify these credit errors and correct them early.

Before you start refinancing, order your credit reports from Equifax, TransUnion and Experian. Under federal law, consumers are entitled to one free credit report per year from any state.

If you discover an error, report it immediately. The agency must remove any lines of credit that you cannot prove are yours.

A survey by the Consumer Financial Protection Bureau (CFPB) found that nearly half of all homeowners had applied for a mortgage quote from just one lender.

Rhb Home & Commercial Property Refinancing

Consumers who received interest rate offers from multiple mortgage providers saw their interest rates reduced by up to 50 basis points (0.50%).

Your current lender or local bank may not offer the best refinancing option for you. Compare the rates and fees of three to five mortgage lenders before choosing one.

This means that you have at least 50% equity in your home. This means it’s money you can use to achieve other financial goals through a cash-out refinance.

For example, a car with a lifespan of five years cannot justify a mortgage with a term of thirty years. You have to pay off that car for more than twenty years, even after you no longer own it.

What Happens When You Pay Off Your Mortgage?

“It goes without saying that if you’re buying a new car, there are often better deals on auto loans than there are on mortgages,” says Jon Meyer, a certified MLO and credit expert at The Mortgage Reports.

Likewise, refinancing your home can be an expensive way to pay for a month-long cruise. And while using home equity to pay off high-interest credit card debt allows you to save every month, you could be paying off that debt for decades.

Homeowners can get more value by investing their assets in home improvements, a college education, or a promising business venture with the proceeds from a cash-out refinance.

Can leveraging your assets deliver long-term returns? If the answer is yes, a cash-out refinance could be your next step.

Refinance Home Loan In Singapore: Your Ultimate Guide

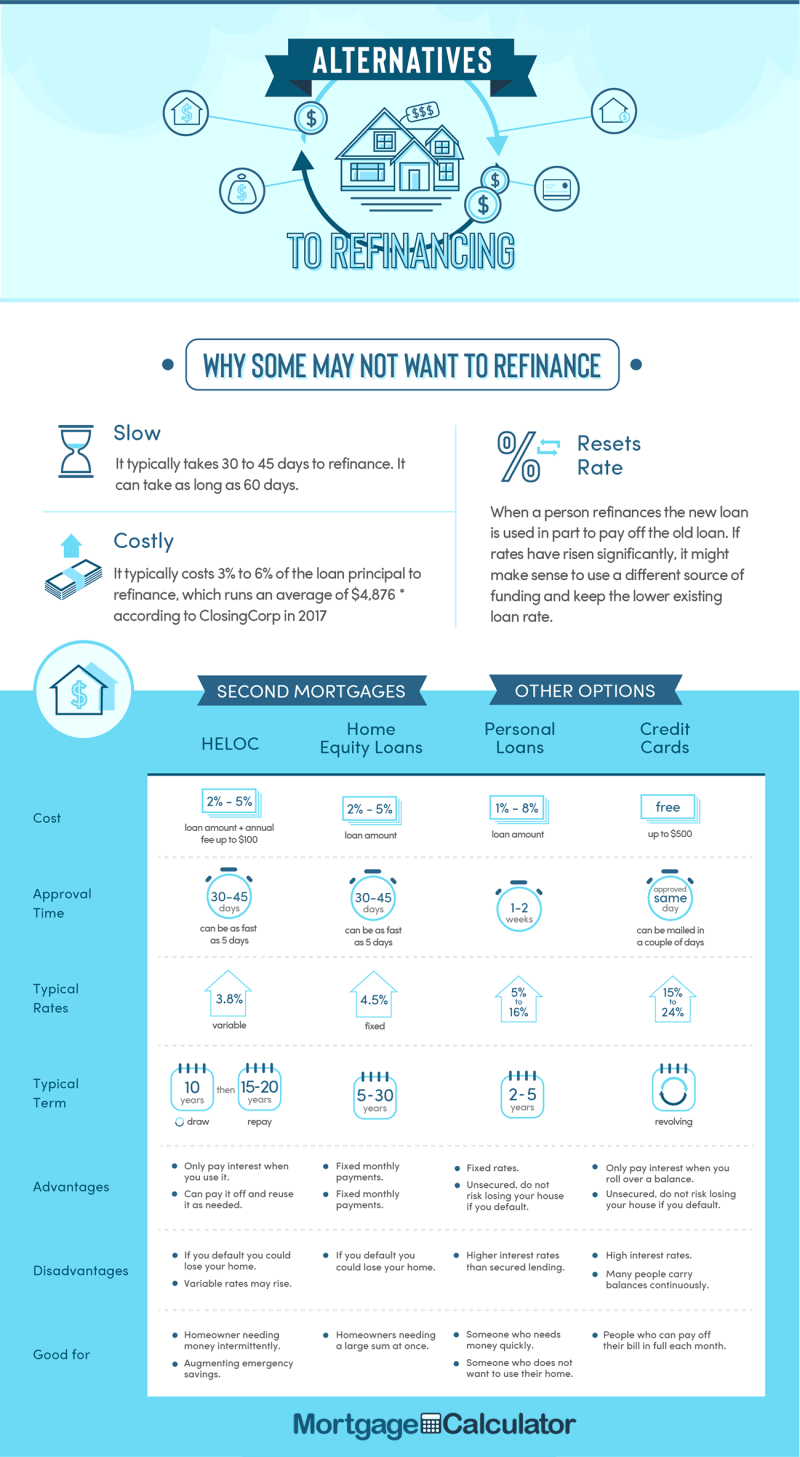

Or, if you’re looking for a short-term loan using your assets as collateral, consider getting a home equity line of credit or HELOC instead of a cash-out refinance.

Refinancing is usually worth it if it can lower your interest rate and payments or provide other financial benefits, such as paying down equity or converting an adjustable-rate loan to a fixed-rate loan.

When refinancing after five or ten years, the term of the loan is often reset to thirty years. Although your interest rate and monthly payments can be significantly reduced, you could still pay more over the life of the loan.

Additionally, unless you find a loan program with no closing costs, you will likely have to pay closing costs every time you take out a new loan.

Reasons To Refinance Your Home

Sometimes for homeowners with limited cash flow, the lowest possible mortgage payment becomes a priority. Perhaps your income has decreased due to divorce, dismissal or illness. In these cases, extending the loan term can be a smart move, even if it will cost you more in the long run.

One strategy that many homeowners use is to refinance to a shorter-term mortgage. That is why refinancing at 15 years is becoming increasingly popular.

Alternatively, you can pay additional principal to avoid renewal.

What happens when i refinance my house, what happens to equity when you refinance, what happens after you sell your house, what happens when you refinance mortgage, what happens to heloc when you refinance, what happens if you refinance your house, what happens when you refinance a car, what happens when you refinance your mortgage, what happens if i refinance my house, when you refinance your house what happens, what happens when you refinance a loan, when you refinance a mortgage what happens